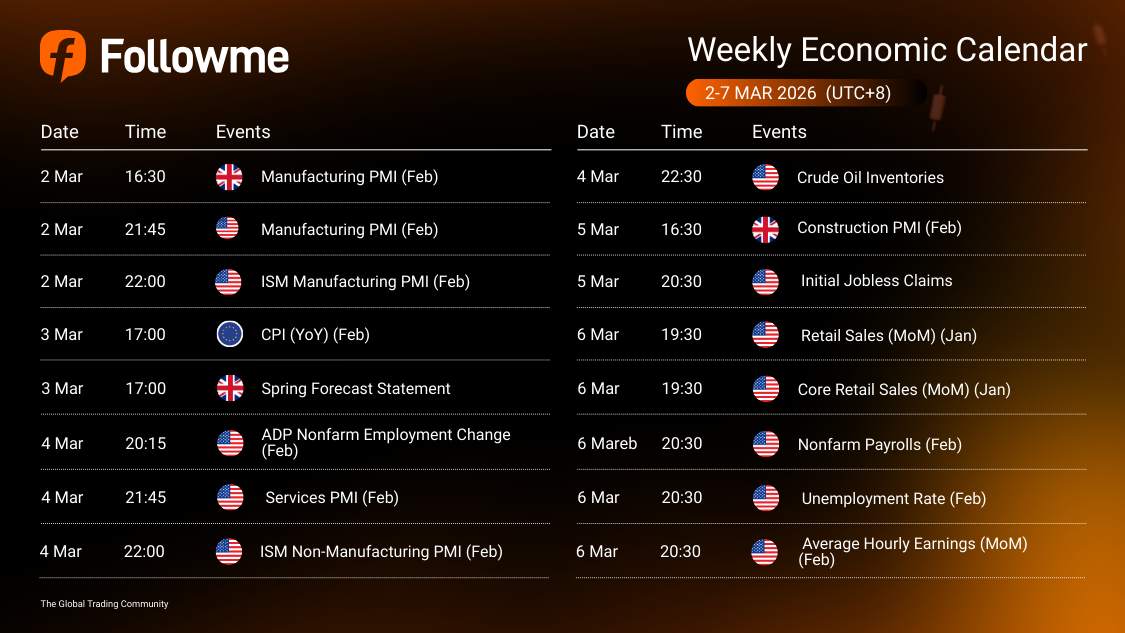

Weekly Economic Calendar: Week of March 2- 7, 2026 (GMT+8)

This week’s macro calendar is driven by a heavy concentration of U.S. growth and labour signals, with the market focus shifting from early-week PMI and ISM activity updates into a powerful Friday cluster of U.S. consumption and employment data.

| Time | Cur. | Events | Fcst | Prev |

| Manufacturing PMI (Feb) | ||||

| Manufacturing PMI (Feb) | ||||

| ISM Manufacturing PMI (Feb) | ||||

| CPI (YoY) (Feb) | ||||

| Spring Forecast Statement | ||||

| ADP Nonfarm Employment Change (Feb) | ||||

| Services PMI (Feb) | ||||

| ISM Non-Manufacturing PMI (Feb) | ||||

| Crude Oil Inventories | ||||

| Retail Sales (MoM) (Jan) | ||||

| Core Retail Sales (MoM) (Jan) | ||||

| Nonfarm Payrolls (Feb) | ||||

| Unemployment Rate (Feb) | ||||

| Average Hourly Earnings (MoM) (Feb) |

| Key highlights: |

🇬🇧 UK Growth Pulse (Manufacturing PMI) on Monday: A first read on UK activity that can move GBP quickly if the number surprises, because it influences how markets price growth momentum and the BoE path.

🇺🇸 Labour Warm Up (ADP Employment) on Wednesday: Often shapes positioning into Friday because it influences labour expectations, although it can also increase whipsaw risk if it diverges from NFP later.

🇺🇸 U.S. Services Engine (Services PMI and ISM Non Manufacturing) on Wednesday: A key growth driver for the U.S. narrative because services dominate activity, so surprises can reprice yields and push USD direction.

🇺🇸 Inflation Via Energy Channel (Crude Oil Inventories) on Wednesday: Large draws can lift crude and inflation expectations, while builds can pressure oil and cool near-term inflation pricing, which then spills into yields and USD cross flows.

🇬🇧 UK Cyclical Check (Construction PMI) on Thursday: A secondary UK growth input that can reinforce or challenge earlier UK signals, so GBP can react if it changes the momentum story.

🇺🇸 Labour Checkpoint (Initial Jobless Claims) on Thursday: A high frequency read ahead of Friday where lower claims usually supports yields and USD, while higher claims can pull yields down and weigh on USD.

🇺🇸 U.S. Demand and Labour Finale (Retail Sales and Core Retail Sales, then NFP and wages) on Friday: This is the week’s main repricing window because demand prints first and then labour and wage inflation follow soon after, so USD can move fast and reverse quickly if the signals conflict.

🟢 Bullish USD Scenario

Manufacturing PMI and ISM hold firm on Monday, supporting yields through growth confidence

Services PMI and ISM Non-Manufacturing stay resilient on Wednesday, reinforcing the U.S. growth narrative

ADP improves versus the prior 22K, supporting labour strength expectations

Initial Jobless Claims come in below 212K, showing labour remains tight

Retail Sales and Core Retail Sales beat the prior 0.00%, confirming demand resilience

Nonfarm Payrolls beat the prior 130K and Average Hourly Earnings stayed firm versus 0.40%, keeping inflation pressure alive

🔴 Bearish USD Scenario

Manufacturing PMI and ISM soften on Monday, pulling yields lower through weaker growth expectations

Services PMI and ISM Non-Manufacturing cool on Wednesday, weakening the U.S. activity narrative

ADP disappoints versus the prior 22K, reducing confidence ahead of Friday

Initial Jobless Claims rise above 212K, signalling labour cooling

Retail Sales and Core Retail Sales miss versus the prior 0.00%, reviving slowdown concerns

Nonfarm Payrolls undershoots the prior 130K and Average Hourly Earnings cools below 0.40%, strengthening the disinflation narrative

🟡 Wild Cards (High Whipsaw Risk)

ADP and NFP divergence can cause traders to get wrong-footed and drive sharp reversals

Friday’s compressed timing with Retail Sales at 19:30 and NFP with wages at 20:30 can trigger two-way volatility

A large crude inventory surprise relative to the prior 15.989M can distort inflation pricing and swing USD rates

Mixed signals, such as strong retail sales but weaker wages, can produce choppy, non-trending USD action

Check out full here: Followme Economic Calendar Tool

Follow Followme for the newest market updates

Tuyên bố miễn trừ trách nhiệm: Quan điểm được trình bày hoàn toàn là của tác giả và không đại diện cho quan điểm chính thức của Followme. Followme không chịu trách nhiệm về tính chính xác, đầy đủ hoặc độ tin cậy của thông tin được cung cấp và không chịu trách nhiệm cho bất kỳ hành động nào được thực hiện dựa trên nội dung, trừ khi được nêu rõ bằng văn bản.

-KẾT THÚC-